When the Crystal Cracked

How Knowledge Fragmentation Became the Binding Constraint on Money Movement

In Jim Henson’s The Dark Crystal, a once-whole civilization is shattered when its source of power — a crystal — cracks. The fracture splits a single race into two diminished halves: one retaining power but losing wisdom, the other retaining wisdom but losing agency. Neither can thrive alone. Only reunification restores what was lost.

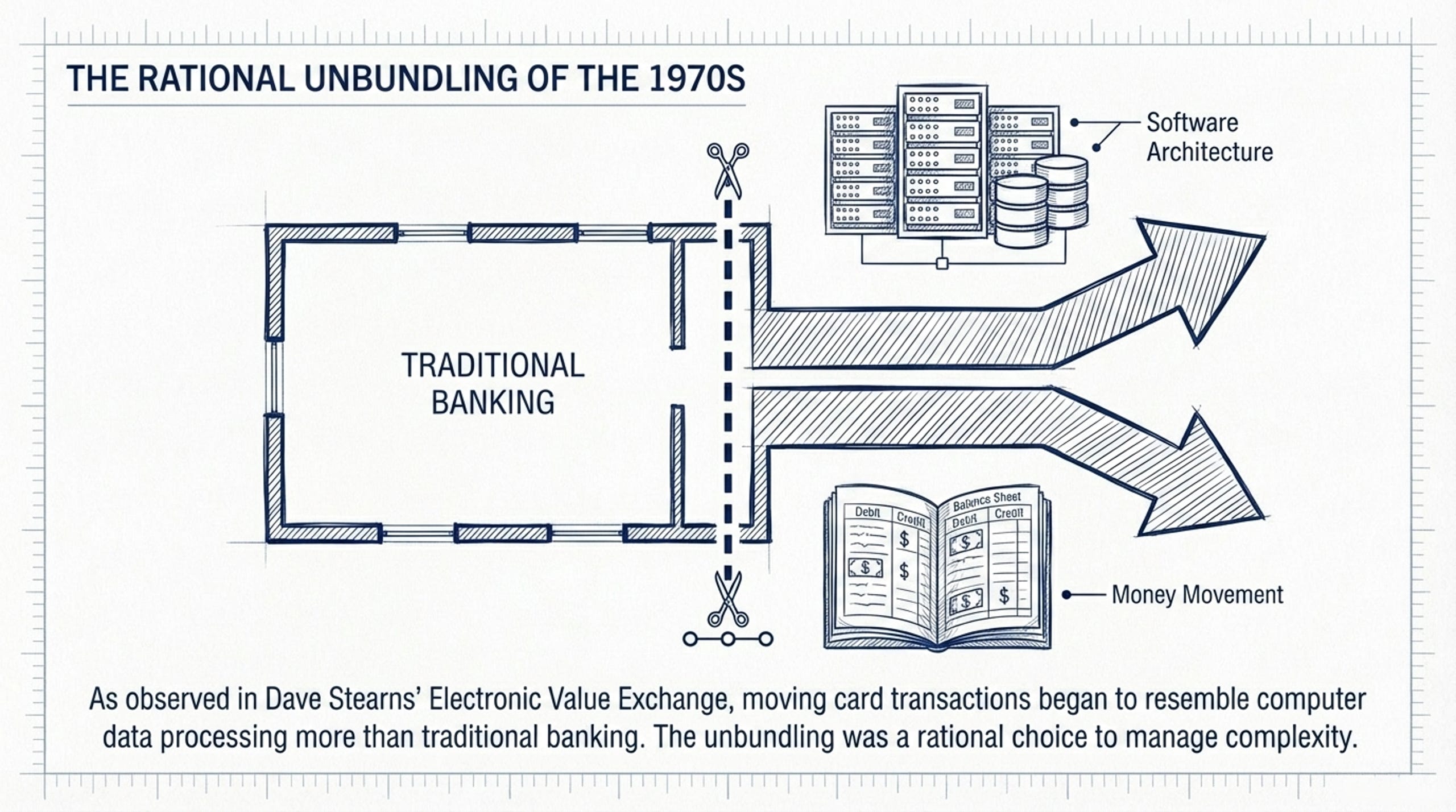

The payments industry has its own cracked crystal.

In Dave Stearns’ Electronic Value Exchange — one of the best histories of the payments industry — there is a quiet observation that explains more about the current state of fintech than most contemporary analysis. As payment card systems became electronic in the 1970s and 1980s, banks increasingly outsourced their processing to third parties. The reason was straightforward: the work of moving card transactions through networks had started to resemble computer data processing more than traditional banking.

This was a rational decision. The credit card industry was trying to do too many things at once — acquire consumers, acquire merchants, build the network, make it run profitably — and the potential margin could support multiple stakeholders. Software engineering and financial engineering are each genuinely complex domains. Better to unbundle them so everyone could stay in their lanes.

But this division created something that has compounded over decades: a structural knowledge gap. Companies and individuals rarely, if ever, understood both scalable software architecture and scalable money movement. The fin and the tech of fintech developed as separate disciplines, with separate career paths, separate vocabularies, and separate mental models.

Staying in Your Lane

And it wasn’t cards alone — consumer-to-business payments — that drove this initial separation. Cards are just one way to move money. ACH, wires, FX, real-time payments, and now stablecoins are others. Each developed its own institutional structures, its own specialists, its own technology stacks.

For a long time, the separation didn’t bind. If your business accepted card payments and paid suppliers by ACH, you could treat those as unrelated operational functions. The flows were simple enough, and the domains distant enough, that nobody needed to hold both in their head simultaneously.

That era is over. Modern businesses rarely use a single payment method, and the methods increasingly feature in the same flow. A consumer-facing company still needs to pay employees and suppliers — using ACH, wires, and increasingly real-time payments. A B2B company may use cards for spend management. A platform acquires card payments from consumers and pays out to merchants through bank transfers, sometimes across borders. An enterprise managing a global legal entity structure may need to route revenue from a single transaction across an IP holding company, a local booking entity, and a central treasury — each in a different jurisdiction, each with different settlement requirements.

As explored in Cloud Clearing, the flows in global commerce have become concatenated (chaining through multiple intermediaries stitching multiple rails), fragmented (proliferating payment rails), and globalized (crossing jurisdictions, currencies, and regulatory regimes simultaneously). This fragmentation is the hidden tax on global commerce. The fragmentation of infrastructure, however, is a downstream consequence of something more fundamental: the fragmentation of knowledge.

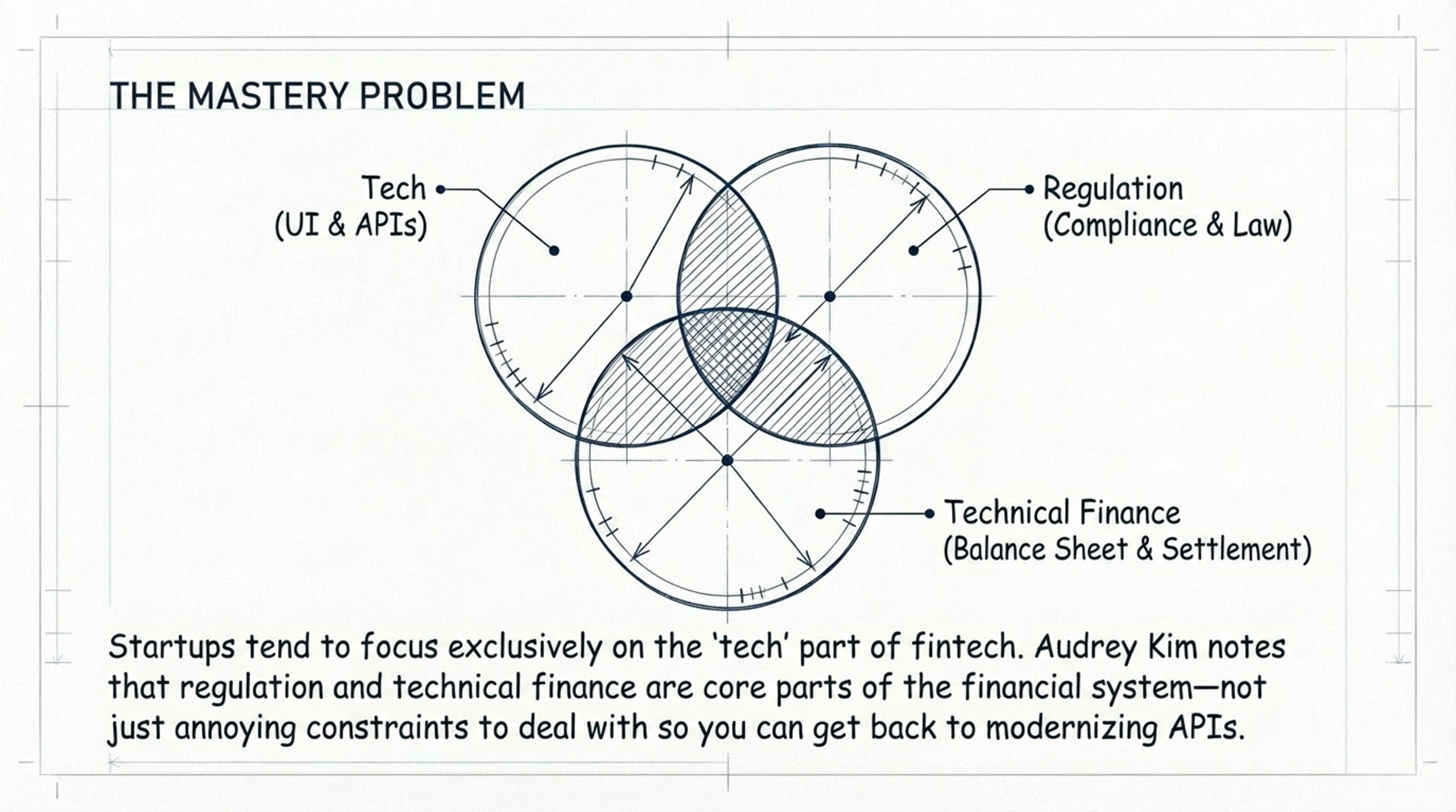

The Mastery Problem

Audrey Kim captured this elegantly:

“Startups tend to focus on the ‘tech’ part of fintech. Compliance and balance sheet are annoying constraints: Deal with them if you have to, so you can get on with the work of modernizing the UI & APIs.

Of course UI and APIs matter. But regulation and technical finance are core parts of the financial system, which have deeper implications than any one feature. Staying perfunctory in those disciplines limits the scope of change you can drive. If you master all three elements, then you can improve the systematic function of how they work together — not just one variable.

Most teams don’t do this because they can’t. Improving the systematic function requires mastery of technology, regulation, and technical finance. Credibility and wisdom take years to build.”

The unbundling of the 1970s and 1980s was rational for its era. But it produced generations of practitioners who are excellent at one domain and perfunctory — Kim’s word is exactly right — in the others. The tech-first founders who treat regulation as an obstacle course and settlement as someone else’s problem. The bank treasury teams who understand duration and liquidity but think of technology as an IT procurement decision. The legal and compliance professionals who can navigate regulatory frameworks but struggle to evaluate whether a proposed architecture actually delivers what it claims.

Each of these perspectives is valuable. None of them, alone, is sufficient for the problems that concatenation, fragmentation, and globalization have created.

And the crystal is still cracking. Blockchain and tokenization have introduced a third fracture line. The crypto and DeFi ecosystem has produced genuinely deep expertise in smart contract design, on-chain settlement, and programmable logic — but often without the institutional finance or regulatory knowledge to deploy it safely. Meanwhile, banks have decades of battle-tested governance frameworks — three lines of defense, model risk management, operational resilience — but struggle to evaluate the code that increasingly is the policy.

Stuart Cook put this well in a recent article: financial institutions need people who can read both a Solidity contract and a Basel III capital requirement and understand how they interact. That talent barely exists today. The original unbundling separated software engineers from financial engineers. Blockchain has added a third population — protocol engineers and smart contract developers — who speak neither of the other two languages fluently, and whose domain neither of the other two populations can easily navigate.

This matters for payments specifically because tokenized deposits, stablecoins, and on-chain settlement are not hypothetical anymore. JPMorgan’s Kinexys platform has processed over $2 trillion in notional value. Banks from BNY to HSBC to Goldman Sachs are building tokenized infrastructure in production. But as Cook observes, the governance gaps — who controls the logic that moves money, what happens when code executes correctly but produces an unintended outcome, how you audit a system where policy is code — are real and largely unsolved. The hardest part of tokenization isn’t the technology. It’s everything around it.

The knowledge gap that opened in the 1970s hasn’t just persisted. It has widened, with each new rail and each new technology adding another discipline that practitioners must master — or find partners who have.

The cliché version of this observation is that every company will be a fintech and every bank will be a technology company. There is something to these claims, but they obscure more than they reveal. “Being a fintech” is not a binary state. The question is whether you can operate at the intersection with sufficient depth in both domains to see opportunities that are invisible from either one alone.

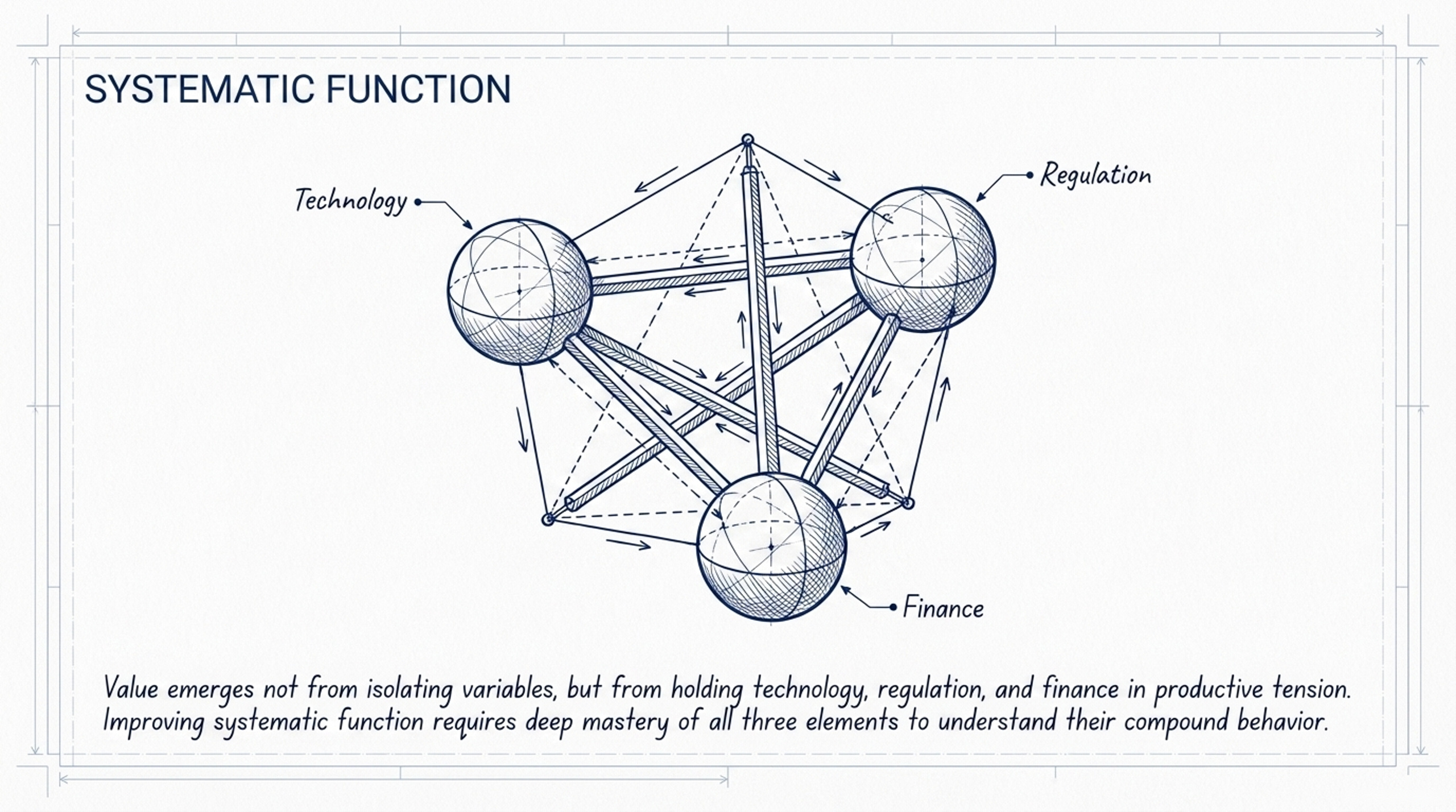

The way money moves through a concatenated, fragmented, globalized flow is not just a technology problem (better APIs, faster rails) or just a finance problem (cheaper funding, better FX rates). It is a systems design problem that spans both domains. The settlement timing, the netting opportunities, the liquidity implications, the regulatory constraints, the software architecture that makes it all programmable — these interact, and the interactions are where the value is. That is what Kim means by “systematic function”: the compound behavior that emerges when technology, regulation, and technical finance are held in productive tension rather than addressed in isolation.

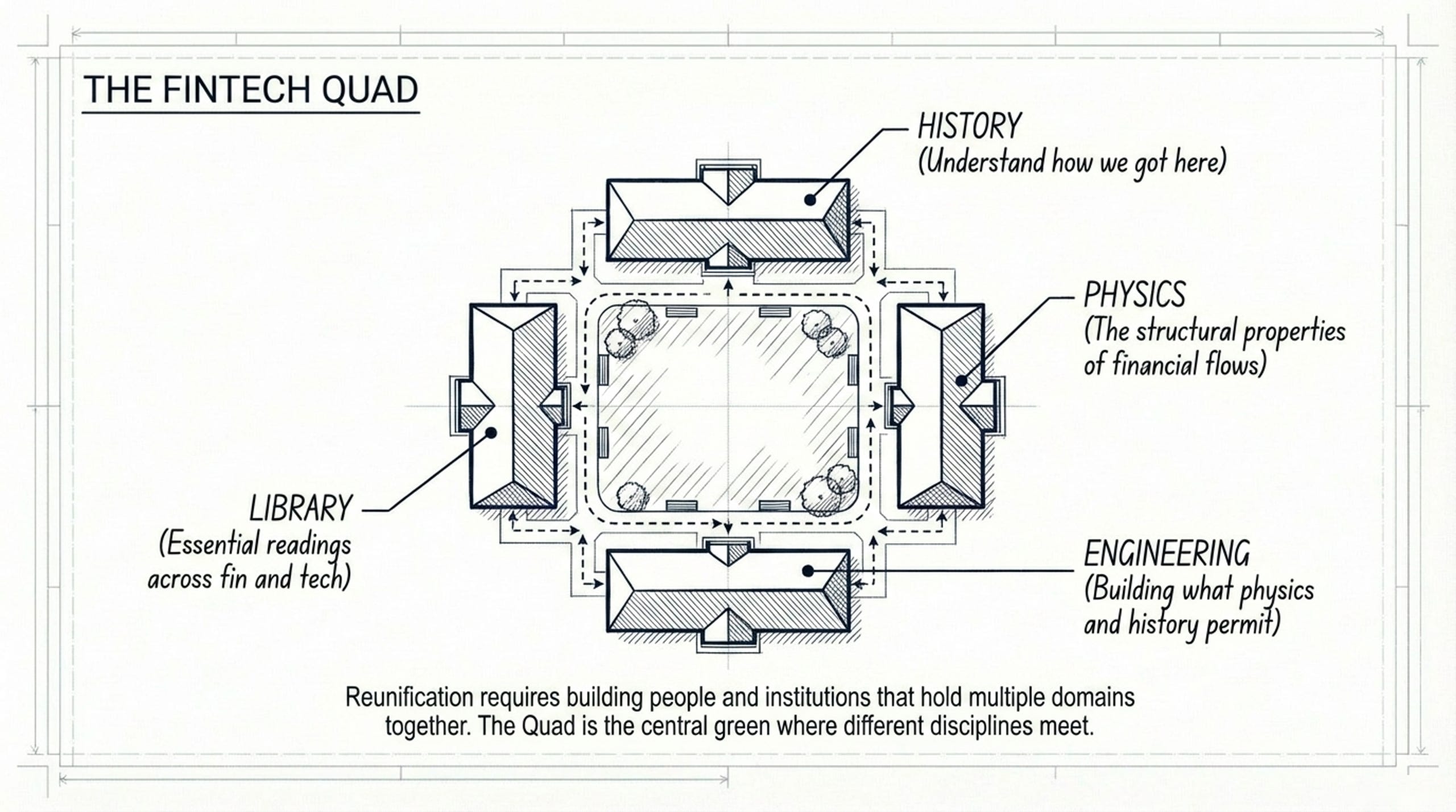

The Quad

The history of the payments industry is a history of unbundling — of a crystal cracking and the resulting halves drifting further apart with each new rail, each new technology, each new regulatory regime. The tech side retained the power to build at scale but lost the wisdom of how money actually works. The finance side retained deep institutional knowledge but lost the agency to reimagine the infrastructure. Each half developed its own expertise, its own career paths, its own languages — and each became more perfunctory in the other’s domain with every passing decade.

But there is reason to think the next chapter may be about reunification. Not by collapsing everything back into banks, but by building people and institutions that hold multiple domains together.

One reason for optimism: the same AI tools that are disrupting software development may also compress the timeline for cross-domain mastery. Furnaces and Flight Simulators explores how AI could enable what Catalini, Hui, and Wu call accelerated talent discovery — as execution costs collapse, individuals can cycle through domains and problems at a pace that was previously impossible. The traditional decade-long apprenticeship assumed expertise could only accumulate through sustained exposure to a single domain. When AI handles more of the execution, practitioners can range more widely, building the kind of cross-disciplinary fluency that Kim describes as the prerequisite for improving systematic function. The knowledge gap that took fifty years to open might not take fifty years to close.

This is what Fintech Quad is about. The quad — like the central green of a liberal arts college — is the place where different disciplines meet. History, to understand how we got here and why things are the way they are. Physics, to understand the structural properties of financial flows and what they permit. Engineering, to build what the physics and history suggest is possible. And a library of essential readings across both the fin and the tech — because the crystal won’t heal itself. It takes serious, cross-disciplinary study, and a willingness to learn the other side’s language.

In the film, the crystal is restored and both halves are made whole, to ‘replenish themselves and cheat death again’. Immortality may be a stretch for fintech. But the additional dimensionality that comes from truly understanding technology, regulation, and technical finance together — from seeing the system rather than just one variable — is what unlocks the next order of magnitude: faster, cheaper, and more inclusive money movement at global scale.

Further Reading:

Dave Stearns, Electronic Value Exchange: Origins of the Visa Electronic Payment System — the best history of how card payments actually developed

Audrey Kim, “The Three Elements of Fintech” — the mastery framework referenced above

Stuart Cook, “Programmable Money Without Governance Is Just Programmable Risk” — why the hardest part of tokenization isn’t the technology

Perry Mehrling, Economics of Money and Banking (Coursera / Columbia) — the best course on how money actually works